Okay, so I’m sure you’ve probably heard of that Barefoot guy, right (his name’s Scott Pape)? Maybe you’ve been meaning to read the book, but just never got around to it. Or maybe you just haven’t had to time to prioritise reading it, but still want to enjoy the perks anyways.

I’ve got you!

Here is the complete Barefoot Investor summary, so that you can finally take control of your finances and be FREE! It really doesn’t matter how much you earn or how old you are – everyone has the ability to be a Barefoot Investor.

I know, money and budgeting can feel totally overwhelming. Let’s face it, out of all the things we’re taught in schools, basic money management is never covered (and it should be!).

We’re living in a society of adults who are running their own households at a loss because they simply don’t know how else to do things.

You don’t have to be a super budgeter or an accountant to incorporate the barefoot steps into your everyday life. In fact, it’s so easy, you can even have fun with it – trust me!

If you’re ready to be financially smart and take control of your incomings and outgoings, the Barefoot Investor is a life-changing way to live.

Have a browse through this Barefoot Investor summary and get your money working for you right now, instead of the other way around.

Does that mean you don’t have to buy the book now?

Well, technically no, you don’t need to. You could just scan through this summary and be on your way. But I most definitely recommend investing in your own copy to help inspire you and keep you on track with the steps. Also, you should lend it to anyone who is willing.

Now, let’s get into it!

We are a participant in the Adventure Awaits and eBay Partner Programs, affiliate advertising programs designed to provide a means for us to earn fees by linking to ebay.com and other affiliated sites. We may earn a commission from your purchases at no extra cost to you. For more information, see our disclosures here.

Barefoot Investor Summary – INTRO

Are You an Alpaca or a Groundhog?

Alapacas:

- Fierce go-getters who will take the bull by the horns and do what it takes to be successful and better themselves.

- Work their butts off to pay out their debts, they’ll buy a cheaper car if the current one is too expensive to run and they’ll have no qualms in cancelling Netflix or Foxtel if they’re not getting used enough.

- Take full responsibility for their financial situation and will get ahead, whatever it takes.

Groundhogs:

- Sit back and complain about the way things are, but never actually do anything about them to bring change.

- Full of excuses, “I don’t earn enough,” “I don’t understand budgeting,” “The cost of living is too high.”

- Want the magic solution without having to do any of the work.

- Take no responsibility for their financial situation and will never get ahead.

Question: Are you an alpaca or a groundhog? The fact that you’re reading this post probably means you’re an alpaca.

Answer: Most people are groundhogs.

The Barefoot Steps

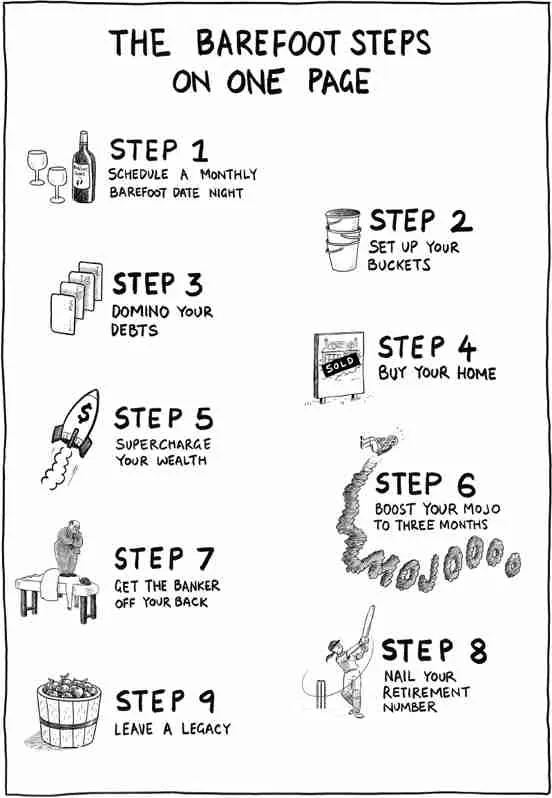

Here are the Barefoot Investor steps:

- Set a monthly ‘money’ date night (even if you’re single!)

- Set up your buckets, super & insurance

- Domino your debts

- Buy your home

- Increase your superannuation

- Save 3 months of living expenses for emergency

- Pay off your home

- Pinpoint your retirement figure

- Set up what you can for the next generation

Barefoot Investor Summary – PLANT

STEP 1: Schedule a Monthly Barefoot Date Night

Whether you’re single or partnered up, you need to schedule one weekly Barefoot Date Night for the next five weeks. Then, you’ll be penning in a Barefoot Date Night once a month, every month, forever more.

Scott Pape reckons that financial chit chat is always better with garlic bread and wine!

The first five nights are to plant your apple tree and set up your finances.

The monthly date nights after that are to keep watering the tree and observe it’s growth.

DATE 1 – Barefoot Banking

- Set up 2 x Everyday Accounts

Jump online (you can literally do this on your phone while you’re waiting for the entree) and set up two ING Orange Everyday accounts. They have zero fees, ATMs included.

Name them ‘Daily Expenses’ and ‘Splurge.’

Keep in mind that one of them will need to have $1,000 per month deposited into it. Make that the ‘Daily Expenses’ account and get your income deposited into it.

Get two cards sent out for each account (if you’re partnered). One of each for you, and one of each for your partner.

2. Set up 2 x Savings Accounts

Open two ING Savings Maximiser accounts that are linked to the Daily Expenses account.

Name them ‘Smile’ and ‘Fire Extinguisher.’

3. Set up 1 x Mojo Account

With a completely separate financial institution, set up one bank account. The idea is to make the money in this one a bit harder to access.

Name it ‘Mojo.’

This is the ultimate emergency account, only to be used when you need a Get Out of Jail Free Card (e.g. when the house burns down or the car dies).

You need an initial deposit of $2,000 for this account. According to Scott, this is absolutely imperative. What if you don’t have a spare $2k lying around (cos let’s face it, if you did, you wouldn’t be reading The Barefoot Investor)? It’s time to raid the house, the garage and the shed and sell whatever you can on eBay, Marketplace or Gumtree. Do whatever you can to get that $2,000 starter figure.

This account is the backbone of never having any financial emergencies.

DATE 2 – Superannuation

Invest in a super fund that charges super low fees. How do you figure that out?

Google ‘[the name of your super fund] + PDS’

Open up the document and scroll down to the ‘Fees and Charges’ section.

You want a superannuation fund that charges less than 0.85% a year in fees (total).

Scott Pape highly recommends Hostplus Indexed Balanced Fund. At the time of writing they only charge 0.07 perfect in investment management fees (i.e. 7 cents for every $100 invested), plus a $78 yearly admin fee.

If you’re not happy with your current super fees, it’s time to open up a new fund and start rolling over all existing funds into the new one.

DATE 3 – Insurance

RULE 1: Only insure against things that’ll financially wipe you out

This would include things like a house fire or burglary, car accident, sickness, emergency hospital visits, not being able to work, disability or death.

RULE 2: Opt for a higher excess

When setting up an insurance policy, opt for a higher excess, which will bring your annual premium down. If you do need to claim on insurance, you will now have your Mojo account to pay for that excess – no need to stress!

RULE 3: Renegotiate your insurance premiums every year

When your insurance policies are up for renewal, don’t just let it roll over and continue paying the going rate. Ring the company and ask for a better deal. Google better deals and let them know you’re going to move elsewhere if they can’t offer anything better.

PRIVATE HEALTH INSURANCE

General rules of thumb for private health insurance in Australia:

- If you’re under 31 years old, you probably don’t need it

- If you earn under $90,000 as a single – don’t need it

- If you earn under $180,000 as a family – probs don’t need it

However, if you earn over those figures, you’ll be getting slumped with the Medicare Levy Surcharge (if you don’t have private cover). So, you may as well spend that money on private cover and get the benefits.

The recommendation is to opt for the top level ‘comprehensive’ private hospital cover. But, don’t waste your money on the ‘extras’ or ‘combined’ cover. You have a ‘Mojo’ account for the odd chiro or physio that you may need throughout the year.

Compare health insurance products at PrivateHealth.gov.au.

INCOME PROTECTION

- Check that you’ve got ‘life cover,’ ‘total permanent disability’ and ‘income protection’ with your superannuation fund. Most have a default level that’s included.

- Get a quote from your super fund for having insurance to cover 12 times your annual salary of combined life and TPD.

- Get an income protection quote for 75% of your wage until you reach the age of 65.

- Find out how much extra you’d have to contribute to your super each month to cover the extra insurance (so it’s not eating away at your balance).

- Hook it all up if you can afford to do so.

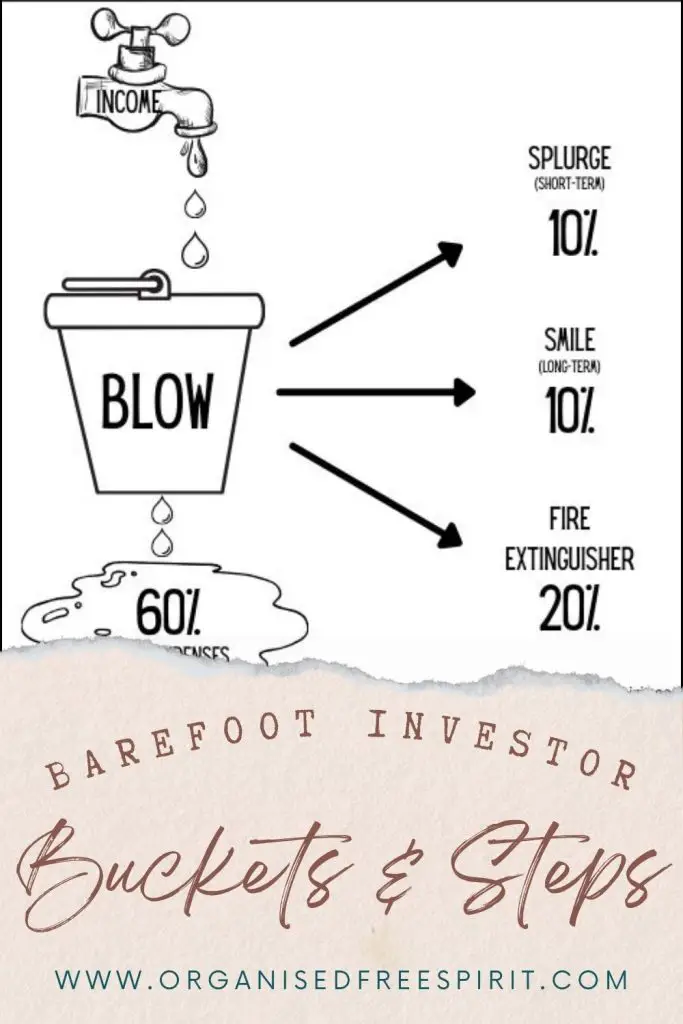

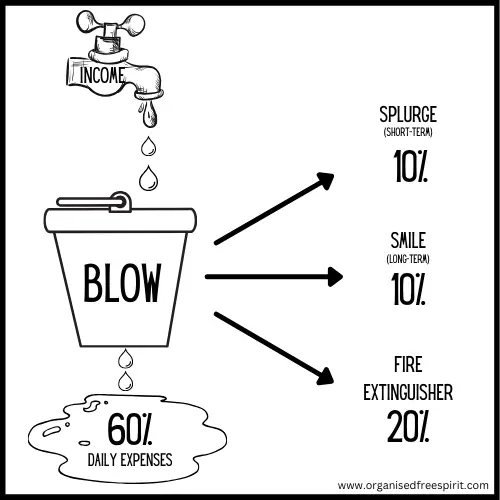

STEP 2: Set Up Your Buckets

BLOW Bucket

Get your income deposited into your ‘Daily Expenses’ account. This is where 60% of your money will remain for all living expenses (rent/ mortgage, food, fuel, bills).

Splurge (10%)

Then set up an automatic transfer of 10% into your ‘Splurge’ account every time you get paid. You can even write ‘Splurge’ on the corresponding bank card and leave it in the front of your wallet.

Smile (10%)

Now set up an automatic transfer of 10% into your ‘Smile’ account for every time you get paid. This one is a savings for bigger goals (like holidays etc.).

It doesn’t have to be 10%, that’s just a guide. Consider what you’re saving for, how much that would cost for the year, then break it down into weekly/ fortnightly/ monthly increments (depending on what your pay cycle is).

Fire Extinguisher (20%)

Lastly, set up an automatic transfer of 20% into your ‘Fire Extinguisher’ account. ‘Fire Extinguisher’ is specifically for putting out financial fires, such as:

- Paying out credit cards

- House deposit savings

- Paying out mortgage

MOJO Bucket

Remember, the ‘Mojo’ account is that one that you set up with a completely different bank and did everything you could to get the $2,000 start-up figure.

This is only for emergencies like losing your job, getting sick, having a car accident and needing to pay the excess or your phone dies etc.

GROW Bucket

The ‘Grow’ account is all about long-term growth and investments (shares, property etc.). At this stage, getting your super sorted is step 1.

DATE 4 – Work Out Your Household Figures

Now it’s time to crunch all of your household numbers. Write down all of your costs and expenses so that you can have a visual of what life actually costs you, as well as how much you need for the 10-10-20 buckets.

STEP 3: Domino Your Debts

Domino-ing your debts is all about attacking the smallest debt first, then moving on to the next and so on until you’re debt-free forever!

Key points:

- Credit cards suck – you don’t ever need one with Barefoot savings!

- Don’t waste your money paying off a HECS-HELP debt, it’ll do its own thing once you’re earning over $55,874 per year.

- Your car should always be worth less than half of your yearly income – and you should be paying cash for it from savings.

DOMINO 1: Calculate

Write down every, single one of your debts into a table like the one below. Think toll fines, loans, credit cards etc. (all except HECS and Mortgage).

| Name of Debt | Total Amount | Interest Rate | Monthly Minimum |

|---|---|---|---|

DOMINO 2: Negotiate

Ring each credit card provider one by one and negotiate a better interest rate and lower annual fees.

Option two is to do a 0% interest balance transfer to a different credit card company that’s having a ‘deal.’ This is only worthwhile if you cut the thing up and actually paying it off within the interest-free time-frame is reasonably possible.

DOMINO 3: Eliminate

Cut up every, single credit card (never to be used again) and post a pic on the Barefoot Investor Facebook page.

DOMINO 4: Detonate

Now it’s time to start paying down the debts from smallest to largest (in balance, not interest rate). The simple reason is that smaller debts are going to bring you a quicker sense of achievement, hence building your self-esteem as you go.

Use the same table as what you used above, but this time, write the debts in order of smallest to largest. That is your order of dominos to attack.

| Name of Debt | Total Amount | Interest Rate | Monthly Minimum |

|---|---|---|---|

Paying down debt is considered a ‘financial fire,’ which means you can use the 20% that you’re putting into your ‘Fire Extinguisher’ account to whack straight onto the smallest debt until it’s extinguished. Then move onto the next debt in line.

Don’t forget to keep paying the minimum monthly repayments on all of the other debts out of your ‘Daily Expenses’ account to avoid defaulting.

DOMINO 5: Celebrate

Once you’ve paid out that first debt, head out into the backyard, burn the bill and celebrate!

Then the next day, shift your focus to the next debt in line. When that one’s paid out in full, have another bill-burning celebration. It’s important to congratulate yourself with each and every win.

DATE 5 – Domino-ing Debts

For the final date (before moving them to a monthly affair) it’s time to write down all of your debts in order of smallest to largest.

Ring each credit provider and negotiate a better interest rate, then cut up the credit cards and post your pics on the Barefoot FB page!

Barefoot Investor Summary – GROW

DOUBLE YOUR INCOME

Next in the Barefoot Investor summary, we’re going to explore ways to increase your income while still plugging away at your day job.

- Do freelance work on the side.

- Make yourself invaluable at work by regularly helping other departments and people of influence, plus work for free – often results in pay rise/ climbing the ladder.

- Research your job description and go into your annual Performance Review equipped and eager to do a 200% job over the coming 12 months.

- Turn a hobby or passion into a side hustle.

STEP 4: Buy Your Home

Basically, you’re going to need 20% deposit for your house purchase, to avoid the ‘waste of money’ lender’s mortgage insurance.

Once you’ve domino-ed and cleared all of your debts, that 20% of your income that was going into the ‘Fire Extinguisher’ account, is now savings for your house deposit!

Tips for getting your deposit faster:

- Rent a cheaper place while saving

- Increase your income (see above)

- Sell things that you don’t need (maybe even downsize your car)

- Look into First Home Super Saver Scheme, however it’s not for everyone

- Look into the First Home Owner Grant

Work out a ballpark figure of what you’d be spending on your home, then work out how much you’ll need for the 20% deposit.

Now work out how much you can put away towards your home deposit every month, then work out how many months it’ll take you to achieve that goal.

Finally, mark out the number of months on the fridge and cross it off with every month that draws you closer to owning your own home!

STEP 5: Increase Your Super to 15%

After you’ve completed Step 4 and bought yourself a house, now it’s time to increase your super contributions up to 15%. Your employer should already be putting in 9.5% (unless you’re self-employed), so you just need to add in the extra 5.5% to get yourself there.

The process is easy, you just get a Salary Sacrifice form from your super fund, fill it out (opting for an additional 5.5%) and give it to your payroll officer.

Plus, some info on additional investments…

Shares

- Buy shares as a long-term investment.

- Buy when you’ve got the money, sell when you need the money. Otherwise, just let them do their thing and forget about them.

- Pape recommends the Australian Foundation Investment Company (AFIC) for your first share investment. You’ll need at least $2,000 to start.

- Keep reinvesting the dividends (profits) if you don’t need to cash out.

- Use your superannuation to buy shares within the fund and increase your returns.

Property

- Investing in property incurs huge costs all along the way. Not to mention needing to get a loan to fund the investment.

- Investing in a property trust that trades on the Stock Exchange is a smart way to go. No loans, no renters, no maintenance costs, no rental agents, no interest rate increases. BWP Trust is the example used in the book as it was low at the time, but do your homework to find one that is reputable.

Investing for your kids

The best way you can invest in your kids is to arm them with good, solid financial habits. Don’t just hand over a weekly allowance, make them do household chores and actually earn it – just like working in the real world.

Then give them three jars:

- Splurge: to spend on whatever they like, while learning how to budget and shop around for the best value for money.

- Smile: to learn how to save towards the bigger things.

- Give: to learn gratitude and that being wealthy is about giving just as much as receiving.

For the older kids who have an actual job, instead of handing over a set of empty Chicken Tonight jars, set up three bank accounts with them.

When it comes to investing for your kids’ future or having a nest egg to pass over to them, here’s the run down:

- Don’t invest in a bank account, invest in shares.

- If you earn under $37k per year – buy shares in a low-cost listed investment company (LIC) on behalf of your child. Note: you’ll need to declare income from shares in your tax return.

- If you earn over $37k per year – buy into investment bonds. No need to declare them as income, tax is paid within the bond.

STEP 6: Boost Your ‘Mojo’ to 3 Months

Remember, the ‘Mojo’ account? That one that had $2,000 in it?

The next step in the Barefoot Investor summary is to increase the money in your ‘Mojo’ account to three months’ worth of living expenses.

This is basically the amount that goes into your Blow Bucket each month x 3.

Now that you’ve paid out all the debts and bought a house, you can use your ‘Fire Extinguisher’ money to fill up your ‘Mojo’ bucket.

This is even better than having private income protection, which often only pays you 3 months worth of wages anyways. Now you’ll have your own ‘income protection’ in case of illness or injury.

Barefoot Investor Summary – HARVEST

STEP 7: Get the Banker off your Back

By this stage, you’ve paid out your debt (except the house) and you’ve got a very healthy-looking ‘Mojo’ account. Now it’s time to focus on the mortgage.

- Don’t get the biggest, most expensive house (in the ritziest suburb) – stick to what you can comfortably pay off.

- Don’t get the ‘extra features’ on your home loan, just stick to the basics.

- Don’t fix your interest rate unless you’re really struggling and need the stability.

- If you have over 20% equity in your home, ring your bank and ask for a cheaper rate (tell them you’re ready to switch to a cheaper bank).

- Pay out your mortgage quicker with your ‘Fire Extinguisher’ account

STEP 8: Nail your Retirement Number

What’s the bare minimum you need for a comfortable retirement before quitting work?

This is your minimum retirement number:

- A paid-off home

- Couples – $250,000 in super

- Singles – $170,000 in super

Obviously this number will rise with inflation as the years go on. The Association of Superannuation Funds of Australia (ASFA) have worked out that the following figures as a ‘comfortable standard’ for retirees who own their own home.

Comfortable Standard for Retired Home Owners

(as at October 2021):

- $63,424 for couples/ yr

- $44,155 for singles/ yr

You can always keep an eye on the ASFA Comfortable Standard and keep adjusting your figure accordingly as you work closer to retirement.

Why $250,000 or $170,000?

These are the maximum amount of assets (not including your home) that you’re able to have and still get the maximum age pension rate.

The current Age Pension rates are as follows (as at October 2021):

- Couples – $37,924 per year (combined)

- Singles – $25,155 per year

You can keep up with the current Age Pension rates at servicesausstralia.gov.au.

So, the Age Pension alone covers 60% of your retirement income straight up and it’s guaranteed until you kick the bucket.

Here’s how your $250k ($170k for singles) gets you up to that ‘comfortable standard:

- You own your home.

- You get the Age Pension ($37,924 or $25,155).

- You draw $12,500 (or 5% of your balance) per year tax-free from your super, which will increase as the years go by.

- You each work a day or two per fortnight to keep active. You can earn combined $13,000 (or $6,500 for singles) per year, tax-free without it affecting your pension.

| Singles | Couples (combined) | |

|---|---|---|

| Age Pension | $25,155 | $37,924 |

| Superannuation | $12,500 | $12,500 |

| Work | $6,500 | $13,000 |

| TOTAL | $44,155 | $63,424 |

So, what happens if you’ve got more than that in super when you retire?

High-five! It just means you’ll be living even better. More money in super is always better. The $250k or $170k are just the minimum figures to work towards for a comfortable retirement.

Your ‘Mojo’ Retirement Bucket

By retirement you should have not just 3 months’ worth of living expenses in your ‘Mojo’ bucket, but 3-5 years’ worth of living expenses.

This will cover you in case the market crashes the day before you retire so that you’re still able to live while it recovers and grows your return again.

The three years leading up to retirement, use your ‘Fire Extinguisher’ account to put in the maximum amount of pre-tax super contributions that you can. Make sure all of this money goes into a ‘cash’ account in your super, not ‘shares.’ This way the money can’t be invested, it just sits there like a bank account.

The rest of your money in super should be invested in shares within your super fund to keep it growing. Get the dividends (profits) to be automatically put into your super ‘Mojo’ bucket so that it’s being replenished all the time.

Final Piece of Advice

The reality is that we’re all going to die. To ensure your surviving loved ones have one less stress to think about, create a folder for them.

In the folder you should include:

- Advisors’ details – accountant, lawyer, financial planner, stockbroker etc.

- Bank accounts & loans – names, numbers, passwords etc.

- Investments – A copy of latest share portfolio, managed fund holdings, superannuation details, property titles etc.

- Insurance policies – house, car, health etc.

- Personal documents – birth certificate, marriage/ divorce certificates, copies of driver’s licence, passport, medicare card etc.

- Passwords – for everything including social media (to close it all down).

- Will – including name of executor and enduring power of attorney.

Conclusion

So now that you’ve read through The Barefoot Investor summary, do I recommend you actually go and buy the book for yourself? Hands down, yes!

While I’ve touched on the main points, there is so much more info in the book to help you and inspire you to take control of your own finances.

You should have it on the bookshelf as a reminder for every time you tick off one of the steps, celebrate, then move onto the next one. You should also lend it out to everyone you know in the hopes that they’ll become a part of the Barefoot family.

To be honest though, only the alpacas will read it and say, “challenge accepted.” The groundhogs will find every excuse under the sun to not even borrow it! But you can’t say you didn’t try.

(eBay)

Next, read The Barefoot Investor for Families summary below so that you can teach you kids the barefoot way from day dot.

| READ: Raising Barefoot Kids → |

▶️ VIDEO: Barefoot Investor Summary (Steps + Buckets)

Pin It