If you’ve already read The Barefoot Investor and loved its simple, no-nonsense approach to money, the next logical step is learning how to pass those skills on to your kids.

That’s exactly what The Barefoot Investor for Families is designed to do.

This book takes Scott Pape’s core money principles and adapts them for real family life — from toddlers through to teens — helping parents raise financially confident, capable kids without turning money into a constant source of stress or conflict at home.

In this article, I’ll break down the key lessons, systems and age-appropriate strategies from The Barefoot Investor for Families, including:

- How to teach kids about money in simple, practical ways

- The bucket system adapted specifically for children

- Pocket money rules that actually build good habits

- How to raise kids who understand saving, spending and generosity

- Why this book focuses more on behaviour than bank balances

Whether you’re starting from scratch or already using Barefoot principles yourself, this summary will help you decide how (and when) to introduce money lessons to your kids — and whether this book deserves a spot on your bookshelf.

And if you haven’t read the original Barefoot Investor yet, I recommend starting there first. I’ve linked my step-by-step summary below so you can build the foundations before tackling the family version.

| 🌿 READ: The Barefoot Investor Summary → |

💡 This post may contain affiliate links (including eBay and Amazon Associates). If you buy through them, I may earn a small commission at no extra cost to you. I only recommend things I trust.

Barefoot Investor for Families Review

The Game Plan:

PART 1 – Three jam jars, three jobs, three minutes per week

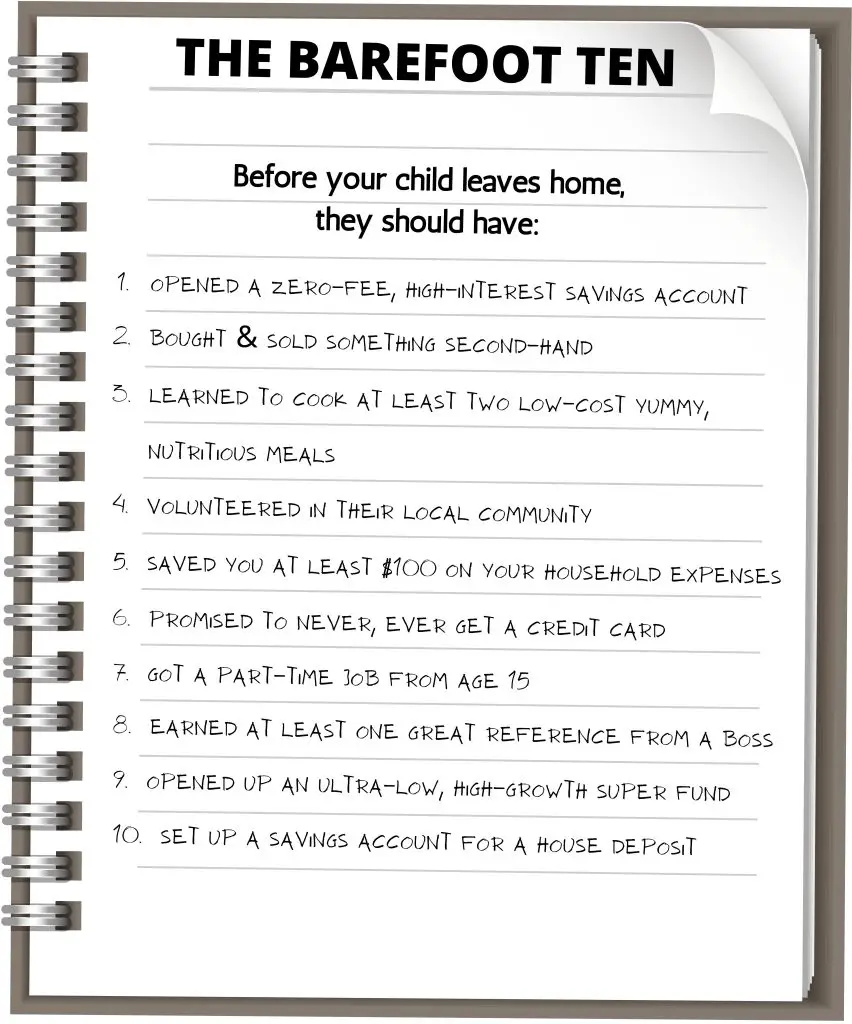

PART 2 – The Barefoot Ten (to tick off with the kids before they leave the nest)

PART 3 – Off and running, plus the ‘Fearless Folder’

Grab yourself a copy of The Barefoot Investor for Families (eBay)

PART 1: First Steps

Three Jam Jars

Introducing the super-simple ‘Jam Jar’ technique.

For this, you’re going to need 3 empty jars (per child). I went with rice syrup because that’s clearly what I go through the most of – use whatever you’ve got!

Each jar is going to have it’s own label:

- ‘Splurge’ – for their everyday spendings

- ‘Smile’ – for saving up to buy things that make them smile

- ‘Give’ – for helping people out

Three Jobs

The biggest lesson for kids to learn surrounding money is this…

“Money comes from working.”

So, rather than kids just being handed over an allowance for doing diddly squat, it’s important that they get paid in exchange for doing jobs.

The Barefoot Investor for Families (aka Scott Pape) reckons that keeping it really simple is the key to success.

Kids will have three jobs each week. If they don’t do them, they don’t get paid.

Here are some examples of jobs that you could get the kids to do, based on their age bracket.

Little kids (up to 7 yrs) – you’ll probably be helping them!

- Clean their room on the weekend

- Take the rubbish out to the wheelie bin

- Help put the groceries away

Tweens & young teens (8 – 14 yrs):

- Sweeping out the garage or back patio

- Empty the dishwasher

- Pull the garbage bins in and out on ‘bin day’

Older teens (15+ yrs):

It’s time for them to get a part-time job. Explain that you’ll keep paying them pocket money (for doing jobs around the house) while they’re applying for jobs. But, once they get a job, or if they refuse to apply for jobs – the pocket money pension gets cut!

Three Minutes

Now, to implement the Jam Jar strategy in just 3 minutes per week.

Minute 1 – Check the kids have done their jobs.

Minute 2 – Count out the coins they’ve earned into their hand.

Minute 3 – Watch them spread the coins out between their three jars (each jar must get some money).

Just to make things even more visual for the kids. Head to The Barefoot Investor for Families resources page and print out The Barefoot Scoreboard. You’ll need one per child, and each one will last one month. So, either print a few or laminate them and get the kids to use a whiteboard marker.

How much pocket money to pay?

The general rule of thumb is to pay $1 per week, per year of age. For example, a ten-year-old would be getting $10 per week. However, the price is totally up to you. It’s all about the life lessons of working hard for their money.

Parents Only Barefoot Date Night!

This is all about getting both parents on the same page with what the goals are for teaching the kids about money and finances.

If you’re single, go with a friend, family member or go solo! Make sure you’re armed with your Barefoot Investor for Families book.

Chat about these four questions:

- Did you get pocket money as a kid?

- What was your first part-time job?

- What did you learn from your parents about money?

- What do you want to teach your kids about money?

Now, flick to the Barefoot Scoreboard and come up with some job examples that the kids can do. Then head to page 15 and read through the Barefoot Ten.

Set a reminder on your phone to print out the Barefoot Scoreboard and make sure you’ve got some empty jars ready to go. Don’t forget to get a pile of coins for their paydays.

The Barefoot Money Meal

The idea of Barefoot Money Meal is to have one family meal per week, where everyone pitches in, the devices are off, and the kids can have their payday.

The benefits include connecting as a family and making memories together. It’s also about sharing existing memories and learning about Mum’s, Dad’s and/ or the caregiver’s childhoods to keep the history being passed down the line.

It’s a family tradition to enjoy and also instil the idea that everyone should help out with preparing the meal, setting the table and cleaning up afterwards.

PART 2: The Barefoot Ten

Open a Savings Account

The first step in the Barefoot Ten is to open a zero-fee, high-interest savings account for each of your kids.

You still want to keep the barefoot jam jars going until they’re 15, but the savings account is somewhere to deposit birthday money and larger sums.

For kids under 15 years:

- Open an online saver that’s linked to your own account

- Nickname it with the kid’s name

For kids 15 years +:

You’re going to open three accounts with your older teen, particularly important once they start working.

‘Splurge’ – A zero-fee Everyday Account (e.g. ING Orange Everyday Youth, but get them to compare and make a choice) for phone credit, clothes shopping, online purchases, etc.

‘Smile’ – A high-interest Savings Account (linked to the ‘Splurge’ account) for a car, overseas trip, gaming PC, etc.

‘Mojo’ – A high-interest Savings Account (with a separate bank) to build up as an emergency savings account so they never have to stress about money in an SHTF (shit hits the fan) situation. Even just $5 per week is a great jump-start into adulthood.

Buy & Sell Something Second-hand

Now it’s time to have a treasure hunt, ‘trash ‘n’ treasure’ style. This lesson is tailored towards learning about how much ‘stuff’ we accumulate and how much it really costs us.

- Set your timer for 2 minutes.

- Tell the kids to go and find one item they’d like to sell, so that they can earn some cash to buy something else they’d rather have.

- Hit ‘go’ on the timer. While the kids are rummaging for an item to sell, grab something of your own to sell (this is a family game).

- Research how much the items cost brand new.

- Research the average prices the items are fetching on the second-hand market.

- Sell them on Gumtree, eBay, Facebook or at a garage sale.

- The kids can use their proceeds to buy something second-hand.

Tip: For kids under 7, you could get them to donate something to the Op Shop, then they can use their ‘Splurge’ money to buy something else second-hand.

Oh, and while you’re at it. Sit down and watch some TV ads together. Nope, I’m not joking. However, instead of letting the brainwashing soak in, you’re going to mute the telly and poke fun at the ads (the Barefoot Investor calls this game ‘Flogglebox’).

Pick apart what they’re advertising and how they’re trying to trick people into buying the product. Talk out if it’s a ‘need’ or ‘want’ item. This will help equip kids for seeing right through the marketing bs as they grow up.

Lessons learnt:

- Money and items don’t grow on trees.

- Put clutter to good use and sell it.

- Buying second-hand is a great way to save money when looking to purchase something ‘new.’

- ‘Stuff’ reduces greatly in value the moment you walk out of the shop.

- Advertisers spend big bucks trying to sell you crap that you don’t need!

Learn to Cook 2 Meals

Get your teen to host a dinner party for the family and invite the grandparents (or other relatives/friends).

Here’s the process:

- Get them to decide who they’ll invite.

- They can decide on a meal that they want to cook and find a simple recipe.

- They need to check the pantry for ingredients and write a grocery list of what’s missing.

- Give them $30 to go shopping for the items (and keep the receipt).

- Prepare, cook and serve the meal, complete with fancy tablecloth and place cards.

- Talk through how many people that meal fed versus if they were to order it in a restaurant. How much more does it cost to order Uber Eats or eat out?

- Everyone pitches in to clean up and do the dishes.

- Congratulate your teen on a successful night. Don’t forget to get photos!

Volunteer in their Local Community

The best way to teach your kids empathy, compassion and build their self-esteem through helping others is to volunteer their time to help others.

World hunger is not just out there in the far world; it’s right here in Australia, too. In fact, there are kids in just about every classroom in the country who’ve gone to school hungry.

Here’s how to empower your kids through the act of kindness and paying it forward.

The Pantry Giveaway

Get the kids to go through the pantry and see what food you’ve got that you can donate to a local community food service. Head to Ask Izzy to find your nearest service.

The Shopping Spree

Next time you’re out doing the groceries, chat with the kids about what food you could get to help people who are hungry. Even better, get the kids to use the money from their ‘Give’ jar to pay for it, then you can donate it to a local community food service.

Volunteer in the Local Community

Get your older kids (tweens and teens) to find a local organisation or group that they can volunteer to help with. It could be a nursing home, animal shelter, food bank, youth group, etc.

Saved at least $100 in Household Bills

This step in the Barefoot Ten is all about getting the kids to negotiate better deals on household bills and save money for you. But, more importantly, get them to actually see how much it costs to run a house and arm them with the skills to reduce their own future costs.

There are three activities, depending on the ages of your kids.

1.Turn the Lights Off (younger kids)

Create a game for the younger kids, focused on turning all the lights, fans and air con/ heating off when they’re not in use. Chase them around the house and see who can switch off the most things!

Make this their new ‘job.’ You could even make it one of their weekly jobs for payday.

2. The Petrol Price Game (tweens)

Whenever you’re in the car driving around, get the tween-aged kids to shout out the fuel prices as you drive past each servo. The idea is to start instilling the monetary savings of finding the cheapest fuel and seeing that the prices are forever fluctuating.

Plot twist: whoever finds the cheapest fuel when you need to fuel up gets a treat from the servo (within the budget you set out).

3. The $100 Challenge (teens)

For the older kids, you’re going to get them to save you money on your household bills… and they’re going to make a cut in the process.

Let your teen know from the get-go how much commission you’re going to pay them for securing you a better deal. Maybe it’s $100, or it could be half of what they manage to save for you.

When a bill is up for renewal (car insurance, house insurance, electricity, gas, phone, internet, etc.), print out the bill.

- Circle the account number, the amount owing and the time period

- Jot down how long you’ve been a loyal customer with that company

- Get your teen to research online for a cheaper deal

- Get them to print/ write down the comparison info (pricing, benefits, terms & conditions)

- They then ring the company and negotiate a better deal, armed with the comparison info they’ve got with the other company

- Celebrate and pay them their commission!

This is an invaluable life skill that most adults don’t get around to doing. Your teen may be so keen on making the quick buck that they’ll be hitting you up to do the next bill when it’s up for renewal.

Promise to Never Get a Credit Card

The sixth step in the Barefoot Ten is focused on teaching kids the truth about credit. They need to know that credit cards, store cards, Afterpay and Zip Pay are all there for the sole purpose of taking their money for crap they don’t need, with disgustingly high interest, for years and years!

It’s not ‘cool’ or ‘mature’ to have a credit card; it’s actually financially dumb. And, with plenty of savings, they’ll never need to borrow for purchases (besides a house), because they’ll always have the money put aside.

I have a personal saying, which I have written on the fridge as a permanent subliminal message for the kids…

“If you don’t have the money, don’t spend it.”

Don’t ask me where I even first heard that saying, but I’ve been churning it out since I was in my early 20s.

Here’s how to teach kids about the evils of credit:

- If you’ve got a credit card, bring out the statement. If not (high-five!), there’s a sample one in the Barefoot for Families book that you can use.

- Circle or highlight the minimum monthly payment and talk about how much is still owing.

- Work out with the kids how long it would take to pay the thing off if you never used it again and only ever made the minimum repayments.

- Work out how old they’d be if that were them, or how old you will be, just to give some context.

- Now, the fun bit is to grab out the blender, throw your credit card in (if you have one) and let the kids see you blend (or cut) it up. If you don’t have one, you could do the demo with an old library card. Or just be honest and explain why you don’t have one.

Credit card myths:

| You need a credit card to get a home loan | FALSE! All the banks need to see for a home loan is a good savings history, no personal debts and a consistent, well-paying job. |

| You need a credit card to get a good credit rating | FALSE! Let’s be honest, they’ve got more chance of forgetting to pay the bill on time or actually paying it out each month. Which means they’ve got more chance of getting a crappy credit rating than a good one. Plus, they’ll be stuck in the credit cycle, which is incredibly hard to break. |

| You need a credit card to buy online | FALSE! A debit card does the exact same thing – but the money comes from their ‘Daily Expenses’ account. No need to pay anything back with interest. |

| You need a credit card for emergencies | FALSE! With a ‘Mojo’ account that has plenty of savings in it (because they’re putting money in there every week), they’ll always have money in case of emergency. And it’s interest-free! |

Get a Part-time Job from Age 15

This is where your kid is really going to be stepping out of their comfort zone and joining the barefoot family – with an income of their own.

Obviously, your teen has no experience and is probably super nervous or maybe even resistant to getting their first job.

A little incentive is that their pocket money days have now come to an end. You can still choose to pay them while they’re applying for jobs, but give it a time limit (such as three months). That way, if they want an income, they need to be responsible for that now.

Here’s how to walk them through the process.

STEP 1 – Make a list of places that you’re happy and willing to ferry your teen to if they get a job there. Think supermarkets, shopping centres and small businesses.

STEP 2 – Head to the Barefoot Investor resources page and print out 2 x ‘Zero to Hero Resumes.’

STEP 3 – Get your kid to fill out one of the resumes themselves, plus you fill out one as well (to help them with ideas when it comes to typing up the real thing).

STEP 4 – At family dinner night, get the teen to read out their answers. Then everybody can help them come up with more ideas for answers based on their own memories and stories.

STEP 5 – Type up the resume and print out 20 copies. Hit the pavement and start handing them out. They should arrive neatly dressed or in their school uniform and ask to speak to the manager at each business. That face-to-face contact is going to leave a lasting impression on the manager’s memory for when it comes to hiring.

Common Interview Questions:

- Why do you want to work for us?

- When can you work (availabilities)?

- Why should I employ you?

- Are you a hard worker?

- Tell me about a difficult situation you’ve faced & how you handled it?

- References (personal & academic).

Earn a Glowing Reference from a Boss

As you’re ferrying your teen to and from work, especially in those first few weeks, use the time to chat about ‘work.’

Talk about the dynamics of the other employees. The ones who are always heads-down, bums-up and get the job done. The slouchers who complain, slack off, and only do the right thing when the boss is watching.

Explain that the boss is always watching, and they know who the hard workers really are. Be the one who shows up on time, always puts in 100% and does it with a ‘hello’ and a smile.

Having a great work ethic always leads to:

- Being ahead of the line for extra shifts

- Pay rises

- Promotions

- Extra opportunities

- Glowing references

Make a HUGE deal out of your teen nailing their first job and making it through the first week. Go out to dinner or have a special dinner at home with the fam. It’s a massive milestone, and shining the spotlight on it will massively increase their confidence. On top of that, it’s a great opportunity to showcase the example to the younger siblings.

As for the reference from the boss. Once your teen has been in their job a while and has proven themselves, they can then ask the boss for a reference, which will be invaluable for them in their resume for future jobs.

Open a Low-Cost, High-Growth Super Fund

Now that your teen is working, it’s time to get their superannuation sorted right from the beginning.

While they could easily fall into the trap of not even considering their super, you now know better, and they will as well.

Most people end up with a whole bunch of super funds that get set up by default with each new workplace. There’s lost super and multiple amounts of fees eating up their retirement fund. It may seem inconsequential now, but over their working lifetimes, that can amount to a loss of almost half a million dollars!

- Get your teen to ask their payroll office if they can choose their own super fund.

- If they can choose their own, get them to have a look at the default fund’s fees online (the fund they were automatically set up with when they started work).

- Now, get them to research and find a fund with cheaper fees (the Total Investment Fee + Annual Fee). Hostplus was one of the lowest at the time of writing.

- Switch to the cheaper fund and roll over any money they’ve already accumulated in the default fund.

- Get them to call their super fund (whether they stay or move) and ask to be invested in the ‘high growth’ option (100% in shares). The recommendation is to invest in ‘index funds.’ If possible, invest 50% into Australian shares and 50% into international shares.

BONUS POINTS: If your teen is interested in further investments, check out Raiz App, where they can set up a share portfolio with a tiny amount of money. Keep in mind, there is a $3.50 per month fee to factor in.

Set up a ‘Home Deposit’ Savings Account

Once your child is working, it’s time to get them to open up one more high-interest savings account. Nickname it ‘Home Deposit.’

Although having a decent house deposit may seem light-years away, this simple act will put your kid years in front of every other kid out there. How many other 15 or 18-year-olds are even thinking about putting away for a house? They’re too busy blowing it all on clothes, booze and food.

It’s up to your teen how much or how often they add to this account, but hopefully, its very existence is motivation enough to keep it growing.

THE BAREFOOT LADDER FUND

If you choose to and can afford to, this is where you help your kids make their way up the impossible barefoot ladder to owning their own home – without giving them an outright handout.

You may decide to match them dollar-for-dollar. Or maybe you’ll give them 10% of whatever they save (10 cents for every dollar).

Given that this can be a long and arduous task, Pape recommends putting the money you want to help them with into the share market.

Share market options:

- Open an investment account in your name and sign up for a managed fund (e.g. Vanguard)

- Use an investment app like Raiz

- If you earn under $37k/yr – buy shares with an investment company (e.g. AFIC – Australian Foundation Investment Company)

- If you earn over $37k/yr – set up an investment bond (don’t need to declare it at tax time as it’s already been covered within the bond). Recommended for investing 10+ years

PART 3: Off and Running

You’ve done it! You’ve given your kids all of the tools they need to be financially fit adults and totally make it in the world.

The second last thing you need to do now, as the accomplished, relieved and proud parents, is to head out to a fancy restaurant and enjoy a victory dinner. If you’re single, take that friend with you who’s had your back every step of the way.

THE FEARLESS FOLDER

Now, for the final task. You will put together The Fearless Folder.

This is your legacy and important documents all rolled into one. The truth is, you’re going to die… at some point. The last thing your family need to be worried about through their grief is how to shut down your Twitter account and cancel the electricity.

Head to the Barefoot Investor website and print out your Fearless Folder Checklist. Then grab yourself a folder and use it to put together copies of all of your passwords, important documents and information.

Don’t forget to add a last letter to your loved ones (either a combined letter, or individual letters).

Finally, grab yourself a fireproof, waterproof safe (like the one below). This is where you’ll store your Fearless Folder, so that no matter what happens, your loved ones will be armed with all of your final information.

Conclusion

Now that you’ve made it through the only kids’ money guide you’ll ever need – The Barefoot Investor for Families.

Let’s recap all that you’ve learned:

- Created 3 ‘accounts’ for your kids (aka Jam Jars)

- Getting them to do household jobs for pay

- Opened a savings account

- Bought & sold something second-hand

- Learnt to cook 2 meals

- Volunteered

- Saved $100+ on household bills

- Promised to never get a credit card

- Got a part-time job

- Earned a reference from a boss

- Opened a super fund

- Set up a ‘House Deposit’ account

Honestly, I reckon even just the basics of the jam jars, working for their money, having a few savings accounts, and zero debt sets your kids leagues ahead of the others.

I hope that you enjoy working through these steps with your kids and tie it all up with a victory dinner at the end!

If you haven’t already got The Barefoot Investor for Families, you should grab yourself a copy. It’s always good to have on hand and refer to as your family grows. Plus, don’t forget to hand it out and spread the word. You could literally change the course of some other kids’ lives.

Okay, now that you’ve got the kids sorted, it’s time to head on over and check out the Barefoot Investor full guide.

Whether you live on a pension or earn $200k per year, every single person can benefit from the steps to be totally in control of their finances and create their own wealth.

More on Kids & Money

Pin It